Trend, Tradeshow Recaps, Industry Insights and more!

Brandon WarrenBrandon Warren

by Brandon Warren, Director of Growth, The Barcode Group

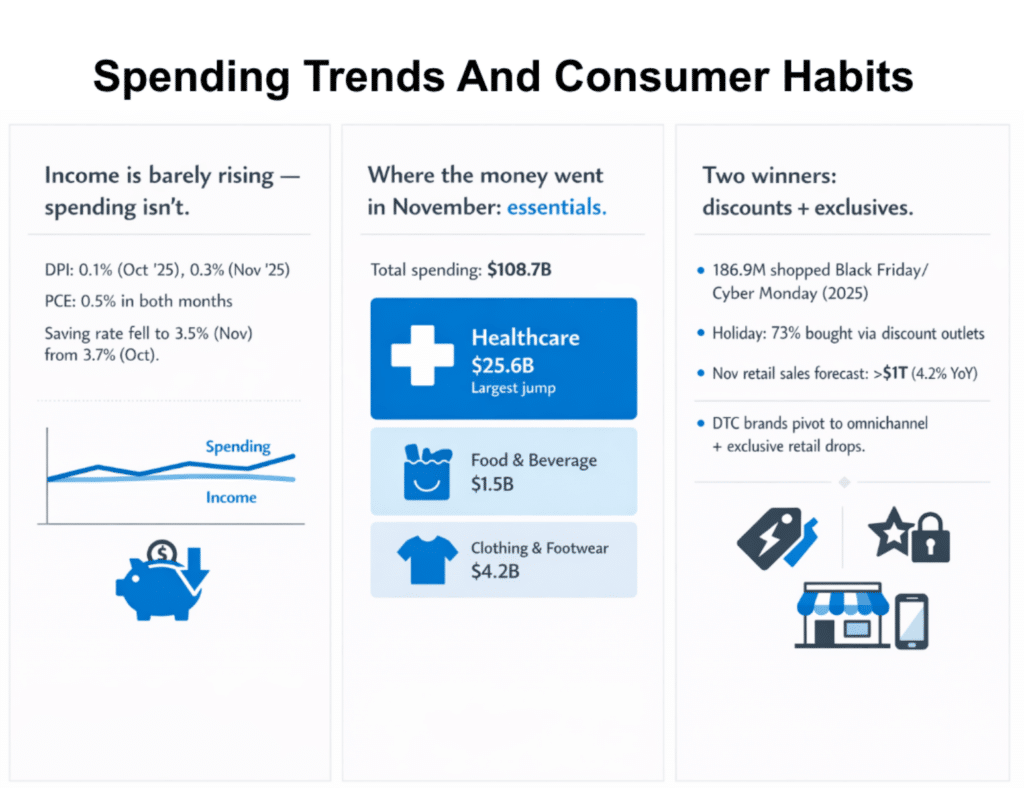

The definition of “essential spending” is undergoing a radical shift for households navigating the persistent gap between stagnant wages and rising costs. Consumer spending remains a vital barometer of economic health, yet recent data from the Bureau of Economic Analysis (BEA) reveals a fragile equilibrium: Disposable personal income rose by a mere 0.1% in October 2025, while the personal saving rate dipped to 3.5%.

The numbers tell a clear story. Americans are increasingly dipping into reserves to maintain standard outlays, forcing a strategic pivot in the retail sector. As prices remain high, the focus for both brands and consumers has moved toward high-exclusivity deals and aggressive bargain hunting.

What is behind these shifts and how do we decode the complex state of affairs currently defining the retail landscape?

Disposable personal income (DPI) was up just 0.1% in October 2025 and 0.3% in November 2025, while personal consumption expenditures increased 0.5% each month, according to the most recent BEA estimates of personal income and outgoings. Data from December 2025 has yet to be published due to the disruption caused by the government shutdown.

The implication is that the typical costs of modern living are rising faster than disposable income. This is , further illustrated by the reduction in the personal saving rate to 3.5% in November, from 3.7% in October. In other words, people have less to set aside from their earnings and must dedicate more for essential purchases.

Overall, consumer spending rose by $108.7 billion in November, with healthcare accounting for the largest portion of this uptick ($25.6 billion). In comparison, the $1.5 billion increase in food and beverage spending showed minimal growth. Clothing and footwear spending in this period rose by $4.2 billion.

That’s why we’re seeing the steady climb of discount shopping as a priority not just for low-income households, but the middle classes as well. A Reuters report on National Retail Federation (NRF) data for Black Friday and Cyber Monday of 2025 crystalizes this. A record-breaking 186.9 million people hit stores during the retail industry’s biggest discounting event of the year, with the NRF forecasting November’s retail sales to have exceeded $1 trillion, up 4.2% year-on-year.

The majority of consumers (73%) made at least one holiday season purchase via a discount retail outlet, whether in-person or online, in 2025, according to data from VTEX shared by Business Wire. Consumers now have greater economic incentives to seek out discounts, and more opportunities to channel their spending accordingly.

A parallel trend worth exploring is the direct-to-consumer (DTC) brand phenomenon and how it is adapting to meet demand for discounts and the importance of omnichannel retail. DTC operators can’t afford to have too narrow a focus, they need to join other retail organizations in diversifying how their products are distributed.

For example, long-time, publicly-traded DTC companies have experienced their stock prices plummeting by at least 50% since their IPOs, according to data cited by Deloitte. The DTC sales model isn’t entirely eroded by this reality. Instead, brands should adopt a more holistic strategy that incorporates aspects of traditional retail.

That’s why DTC brands are striking more exclusive retail deals with long-established brick-and-mortar outlets like Target. Brands that might be suffering from reduced consumer spending can maintain momentum by getting their products on shelves in places that were previously out of reach.

Exclusivity can still be adopted in these contexts, of course. DTC brands may choose to partner with only one specific retail outlet, or leverage options such as timed exclusives, location-specific product drops, and cross-industry collabs. It’s a moment where innovation is rewarded above and beyond raw price positioning and value propositions.

Consumer spending trends that shift toward discount shopping and exclusive retail partnerships with DTC brands can be hard to attribute to a single cause. The economic pressures in the market at the moment are certainly relevant, although they don’t explain everything we’re seeing right now.

Retailers and brands looking to remain buoyant in these challenging, changing conditions must remain flexible and innovative, but also embrace the flexibility and certainty that an omnichannel presence provides. As disposable income and spending flatline, this seems to be the most robust route forward.

We’re constantly gaining industry knowledge: from tips and tricks to back end data, we got crazy amounts of knowledge ready to share with you.

Get access